Notes from Macroeconomics 101

Table of Contents

1. Basic Economics Concepts

1.1 Introduction to Macroeconomics

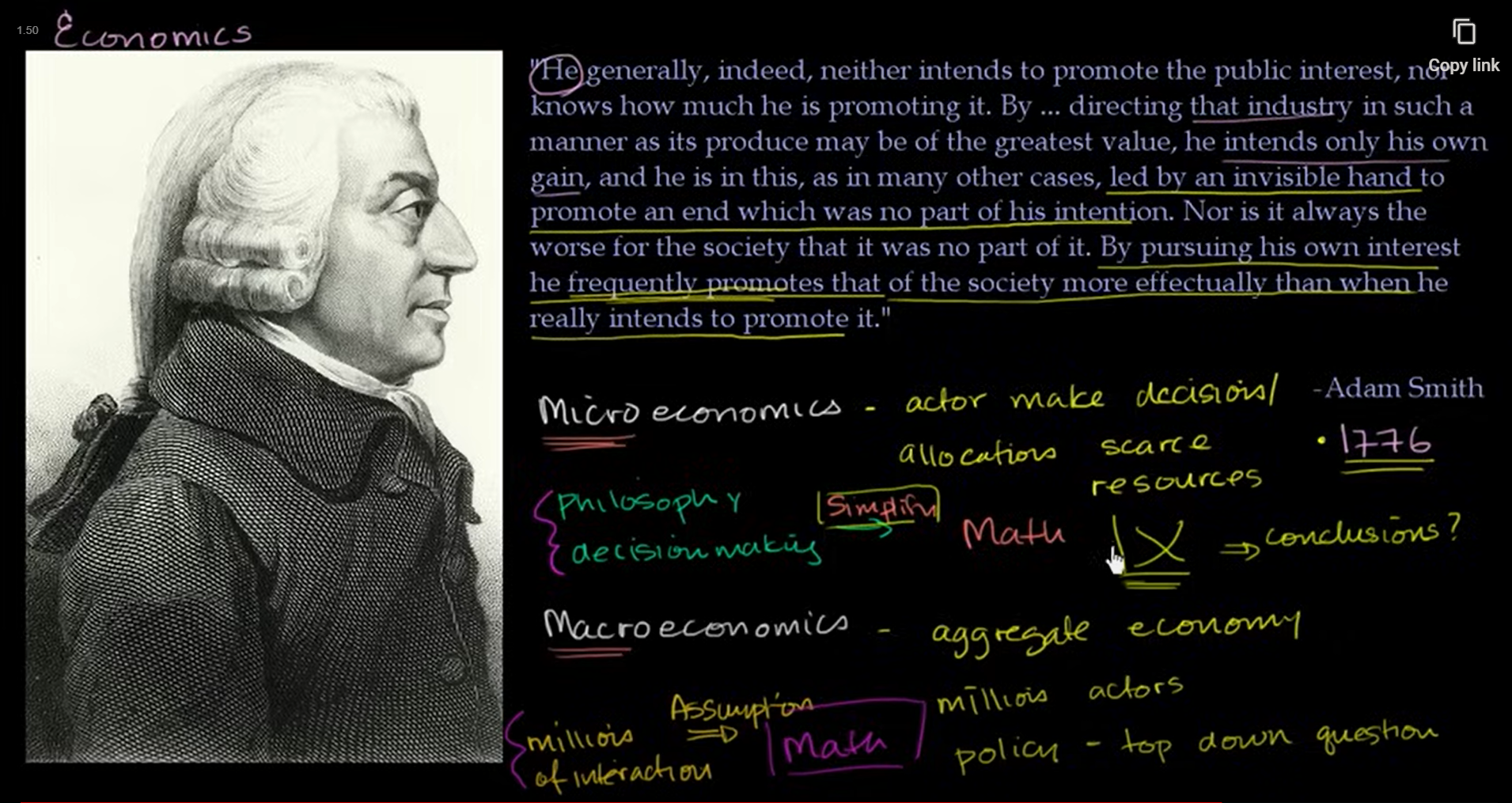

Wealth of Nations by Adam Smith, 1776. Same year as American Declaration of Independence. The concept of capitalism as self interest. The Invisible Hand and self interest of individual actors

| Term | Definition |

|---|---|

| Microeconomics | Focuses on individual actors (firms, people, households) |

| Macroeconomics | Examines the economy as a whole and the collective behavior of society |

Actors make decision / allocation of scarce resources

Sometimes, the mathematical conclusions derived from economics might be wrong, because the assumptions it is based on, or the context that we’re trying to make conclusions about. Specially with macroeconomics, since it has to take millions of unpredictable actors action into consideration. Take it all with a grain of salt.

Intuitions play a key role in macroeconomics.

Economics is not science like physics, it’s open to subjectivity, based on the assumptions we choose to make.

The entire field of Economics is based on the idea of Scarcity

Resources that are not unlimited, and people will use far more of them than there is actually around

Free resources: Infinitely abundant. People can have as much as they want. If one person has it, it doesn’t take from someone else

Economics is the study of how to allocate the scarce resources, and what people have to give up for access to these resources

Labor is also a resource

Oxygen might be, for all purpose, a free resource in Earth. But if we take the same example, to let’s say, Moon or Mars it becomes a scarce resources. Since the supply is limited

| Normative Statement | Positive Statement |

|---|---|

| based on opinions or ethics, can’t be tested (should, wrong, unfair .. are giveaway words) | are testable, even if not necessarily true |

| Example: Paying people who arent' working, even though they could work, is wrong and unfair. The government should raises taxes on the wealthy to pay for helping the poor | Example: Programs like welfare reduce the incetive for people to work. Raising taxes on the wealthy to pay for the government programs grow the economy |

Economic models are a way of taking complicated ideas and events and breaking them down into their most important characteristics. We use models in economics so that we can focus our attention on a few things instead of getting bogged down a lot of details. Simplifying assumptions.

Any economic system must provide society with a means of making choices that answer three basic questions:

- What will be produced with society’s limited resources? (Allocation)

- How will we produce the things we need and want? (Production)

- For whom/How will society’s output be distributed? (Distribution)

Economics straddles between social science and hard science

ceteris paribus: latin phrase. “All else equal" Use to keep variables constant, while making economical assumptions

Another assumption economists make is that economic agents are rational and have an incentive to make decisions that are always in their own self-interests. While in reality human beings often act irrationally, by assuming people, businesses, governments, and other agents are rational decision-makers, and by assuming ceteris paribus_, economists attempt to establish laws and make predictions about how human interactions will affect society.

Command Economy: USSR, communist states. Govt owns/controls factors of production

In extreme command economy, govt even allocates the end results

Market Economy: most of the world economics, like United States. Produce: What does the market need? Result allocation: determined by the market

Points given to command economy: “Fairness” or “Equality”. But this is utopian

Market economy is natural to have some level of inequality. Other points: Innovation, Incentives

There is no perfect market economy. Like healthcare, military

Most economies are in mixed economy.

In economics, capital is defined as the already-produced goods* (tools, machinery, equipment, and physical infrastructure) that are used in the production of other goods or services. A robot on a car factory floor is defined as capital in economics; money you borrow to start your own business is not. _Money is used to invest in the capital but not the capital itself.*